Longevity: The hub of retirement planning

No doubt, when talking to clients about their affairs, and perhaps discussing what lies in their future, you will touch on subjects such as retirement and potentially care later in retirement. Perhaps more so now than ever when the average life expectancy for both men and women in the UK has increased so much.

Whilst longer life expectancy will generally be accepted as positives news, it also presents a number of challenges. Imagine how much simpler planning for retirement would be if we could accurately predict how long each of our clients will live for. If that information were available, we could advise, with certainty, on the best investment strategy, the likely impact of inflation, and how much money to withdraw, and when.

Sadly, this scenario is highly unlikely, unless there is a terminal illness already diagnosed, and it is this uncertainty that gives rise to what we call ‘longevity risk’. The legal profession is trained to be accurate and concise, which is essential when dealing with the law. As such you might well be naturally risk averse but in financial planning for retirement, longevity risk is real, unavoidable and has to be factored in, as certainty seldom exists.

As financial planners we may well need to consider investment strategies which must be influenced by life expectancy. For example, for a client you refer to us in their 70s or 80s, you might expect us to consider lower-risk investment options that are not subject to market volatility. However, that may not be the most suitable option for a younger client whose retirement could last for 35 years, as planning over long periods usually requires exposure to growth assets, which may in turn carry more risk. It is a balancing act for sure!

Another vital factor we must take into account is inflation, which as we all know is currently at generationally high levels. It may not be a major risk over short periods, but it is far more significant over the long term. A we have said, since the pandemic and with the war induced fuel price increases, inflation has risen substantially and remains elevated at the highest level for over 40 years, and with this we have seen volatility and wild gyrations in the financial market. This means that as financial planners, we have to assist clients investing for and in retirement, to come to terms with this new normal and re-evaluate with them how we can prepare portfolios against inflation.

When advising clients approaching or at retirement, we absolutely need to consider life expectancy but this in itself is far from straight forward. There are various measures and pitfalls to factor in. For example, average life expectancy data can be a useful way to track the trends and improvements across the population as a whole, but it is ineffective in forecasting the life span of each individual. Probabilities are more useful in this context. Again, as an example, a 65-year-old woman, according to the ONS, has a life expectancy 87, but also a one in four probability of living to 94, and a one in ten chance of living to 98. For men, the equivalent figures are about two years less.

Life expectancy figures should only be used as a broad indicator because even the life expectancy data offered to us by the ONS Calculator, might lack the precision we need as financial planners. In order for us create the best plan we need to estimate the likely longevity of an individual client and there are various factors to consider:

Socio-economic groupings – The average UK population may not be reflective of your individual clients. Life expectancy rates would vary if socio-economic groupings were considered. If our 65-year-old woman is from a wealthier socio-economic group, and in good health, she has a one in four chance of living to 96, and a one in ten chance of living to 100 according to life company L&G.

The greatest wealth is health – An individual’s health will also impact their life expectancy; both sexes can expect to spend about half of their average life expectancy at 65 in poorer health. Again, these are averages. Someone could remain healthy for 20 years or fall seriously ill in the first year of their retirement. Of course, as financial planners we frequently underpin our clients’ plans with life cover and other protection, so we often have an awareness of induvial and family medical history.

Lifestyle factors – Most people will know someone who smoked, ate unhealthily, drank excessively and lived to a ripe old age. These outliers are just that – they are the exceptions that prove the rule.

Socio-economic grouping, health and lifestyle factors are interrelated, with a growing body of research, indicating that health outcomes in Britain are linked to socio-economic circumstances. These factors are all helpful in informing individual life expectancy, but it’s still an inexact science, which is why we at FB would routinely plan to 100 years.

There is, however, an issue with this approach. According to the Faculty of Actuaries in 2018, a ‘safe’ withdrawal rate from a pension fund at 65 is usually considered to be 3-3.5% each year, but this may not be enough for many people to live comfortably. As financial planners we can include all of a client’s assets and also future incomes. This will of course, include any state pensions due, (we can accurately factor this in thanks to the Government,) and potential any company/defined benefit pension or other assets that they can draw an income from. Increasingly, property equity will become a valuable asset which can, in some cases be used to help fund retirement, via downsizing or equity release.

For more risk averse individuals or indeed simply those wanting their basic regular outgoings covered, we can also consider or include a further option, to reduce the risk posed by longevity, which is a secure guaranteed income. The risk of a client living longer than their retirement savings last may be reduced, or removed, when an income is payable for life. In 2023, annuity rates, having been low for so long, are at a generational high, and must be taken into account, as an alternative or alongside utilising an accumulated pension fund to drawdown an income from. There are also further enhanced annuities we can access for clients who, for health reasons, have a shorter life expectancy.

Our mutual clients are living for longer and choosing more varied retirements than ever before. Although we don’t know how long an individual may live, we can take steps to help them deal with this uncertainty. An element of guaranteed income to underpin a client’s portfolio, and cover essential spending, can certainly be utilised to largely mitigate longevity risk, while providing the freedom to invest a client’s other assets with more flexibility.

Planning for retirement with its unknowns and uncertainties, alongside known expenses and aspirations if complex and far from straight forward. However, at FB Wealth, we have experienced and highly qualified planners, adept in this arena, who by utilising cash-flow forecasting and modelling based on in depth conversations, will help alleviate the stress and anxieties of planning for life after work.

Solicitors are still dominant force in will writing market but …

A new study has recently, happily revealed that traditional law firms/solicitors remain the most popular option for consumers in the wills and probate market.

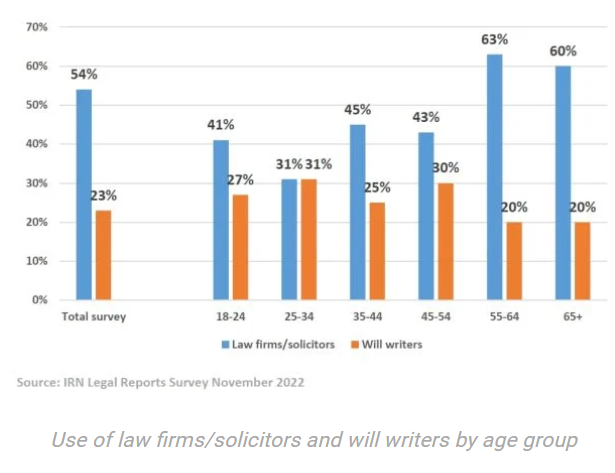

In fact, 54% turned to a lawyer for their will according to 2023’s annual IRN Legal survey. Slightly worryingly though, this has slipped from 56% pre Covid in 2020. The drop can probably be explained, suggests this article in Today’s Wills and Probate, by the increase in will-writing services and individuals. The use of such services, by consumers increased from 19% three years ago to 23% in the latest survey. Advisers at banks, building societies, accountants, or other financial services were used by 5%.

The below graphic shows us the results in more detail, as it breaks it down into the use of lawyers and solicitors, as well as other will-writers by consumer age group.

We see it as Important and gratifying to note that the clients of an age group where we at FB Wealth are likely to be discussing IHT and next generational planning, are still far more likely to use a solicitor over a will-writer. Of course, it goes without saying that we would only refer our clients to properly qualified and compatible solicitors.

Thankfully, the number that decided to go down the ‘DIY’ will route has decreased from 12% to 8% post pandemic, despite the increasing range of online enabling options. The survey suggested that the ‘relatively low cost’ of using real lawyers, for most wills may be behind the factor in the reducing interest in DIY will. We hope this demonstrates and sensible response by the solicitor market to Transparency, and the competition from these new channels. However, as widely reported late last summer, the substantial rise in disputed wills in 2022, up 37%, was in no small part attributed to the previous increase in DIY wills, so this has also hopefully had an impact.

The IRN Legal report, was also very enlightening in digger deeper into why the consumers chose the solicitor/lawyer they did for their will.

- 38% simply returned to a provider they had used for another legal services previously – Good news here for solicitors that there is demonstratable indication of client retention/loyalty.

- 19% were recommended to the solicitor by someone they trusted. (Interestingly this, percentage is far higher in the younger age groups.) This will of course include family and friends but will undoubtedly include trusted advisers such as financial planners like FB Wealth. We believe that the role we can and will play in recommending clients to solicitors we trust and value for wills and indeed LPAs cannot be understated.

- 10% in the survey were persuaded by a charity, which is up 7% from 2018, and this certainly seem to coincide with the increase in charity advertising and promotion in that period.

- Interestingly, only 2% arrived at their provider via a comparison site. This further illustrates our contention, that despite the regulator’s inclusion of such sites, as part of their continued push for Transparency, the personal referral, (described above,) will always outweigh the impersonal comparison site recommendation.

As always, we would welcome a constructive conversation, about where we refer our valued clients for new wills or will reviews and how this might fit in a wider collaborative approach to estate planning and the efficient transfer of wealth to the next generation.

If you would like a CPD certificate after reading this blog, please complete the following information and we’ll send your certificate by email.